As an independent contractor in India, you’re probably familiar with the freedom and flexibility of being your boss. However, this autonomy also brings a unique set of responsibilities and risks. One critical aspect often overlooked by contractors is liability insurance for contractors—a safety net that can protect your business from unforeseen legal and financial challenges.

Importance for Remote Workers and Contractors

Remote work and freelancing have become increasingly common in India. As per some estimates, India has the 2nd largest freelance workforce in the world after the United States, with over 15 million freelancers.

Working independently exposes remote workers to unique professional liabilities compared to regular employees. Without the coverage of an employer's insurance, they are personally responsible for any legal claims arising from their professional work.

Some key professional liability risks for remote workers include:

- Errors or omissions in work deliverables

- Missed deadlines or project delays

- Dissatisfied clients and negative outcomes

- Copyright or trademark infringement

- Breach of contract or negligence allegations

For example, if a freelance software developer's code contains bugs that cause financial losses for the client, they could sue the developer for damages. Professional liability insurance would cover legal defense costs and any settlements or judgments.

Types of Contractor Liability Insurance

Liability insurance comes in different forms, each designed to address specific risks you might encounter. Understanding these types can help you choose the right coverage for your unique business needs. Below, we explore types of liability insurance for independent contractors:

General Liability Insurance

General Liability Insurance is a foundational policy for independent contractors. It provides broad coverage against a variety of common risks. This insurance protects you from third-party claims related to bodily injury, property damage, and advertising injury. For instance, if a client slips and falls at your workplace, or if you accidentally damage their property while on the job, this policy would cover the costs associated with such claims, including legal fees, medical expenses, and potential settlements.

Common situations covered by General Liability Insurance include:

- Damaging a client’s property while on their premises, such as breaking a valuable item or causing structural damage.

- Causing bodily harm to a client or third party, whether through an accident or negligence.

- Legal claims arising from advertising injury could involve defamation, copyright infringement, or misrepresentation in your promotional materials.

Professional Liability Insurance

Professional liability insurance, also known as errors and omissions (E&O) insurance, protects individuals and companies against claims of inadequate work or negligent actions. It covers financial losses caused by alleged failure to perform professional duties. For remote workers and contractors, professional liability insurance is crucial as they provide professional services and advice to clients. Any mistakes or oversights in their work could lead to lawsuits from dissatisfied clients.

Types of Professional Liability Coverage

There are specialized professional liability policies for different professions. Some common ones relevant to remote workers include:

Technology Errors & Omissions Insurance

For technology professionals like software developers, IT consultants, web designers, etc. Covers technology services and products.

Media Liability Insurance

For content creators, publishers, PR firms, etc. Covers intellectual property infringement, defamation, invasion of privacy, etc. in media content.

Miscellaneous Errors & Omissions Insurance

A generic policy that covers various professionals like management consultants, HR consultants, business coaches, market research firms, etc.

Cost of Professional Liability Insurance

Premiums depend on various factors like profession, years of experience, past claims, coverage limits, etc. Typical premiums for freelancers and contractors can range from ₹5,000 to ₹50,000 annually for a ₹1 crore coverage.

Compared to the financial security and peace of mind it provides, professional liability insurance is a worthwhile investment for remote workers. Independent professionals should assess their risks and consult with an insurance broker to choose appropriate coverage limits.

Need for Liability Insurance in Different Professions

In today's dynamic work environment, independent contractors and freelancers are taking on a variety of roles across different industries. However, with this flexibility comes the need to protect oneself against potential risks and liabilities. Liability insurance is essential across a wide range of professions, each with its unique risks:

- IT Consultants: In the tech industry, IT consultants are responsible for implementing systems or providing advice on software solutions. A mistake in coding, a security breach, or even a failed system implementation can lead to substantial financial losses for clients. Liability insurance helps cover the costs associated with such errors, safeguarding the consultant’s business.

- Photographers: For photographers, liability risks can range from accidental damage to expensive equipment to client dissatisfaction with the final product. A dissatisfied client might file a claim for not receiving expected results, or a guest might trip over equipment at an event. Liability insurance ensures that photographers are protected from the financial implications of such incidents.

- Freelance Writers: Freelance writers might face legal claims related to plagiarism, defamation, or errors in the content they produce. Liability insurance provides a safety net for writers, covering legal fees and any settlements resulting from such claims.

- Event Planners: Event planners are responsible for managing various aspects of events, from coordinating vendors to ensuring guest safety. If something goes wrong, like an injury at an event or a vendor not delivering as promised, the event planner could be held liable. Liability insurance helps cover the costs of legal claims, damages, or settlements.

In some professions, liability insurance is legally mandated. This requirement ensures that the client is protected from potential losses or legal actions that might arise from the contractor's work. For example, certain sectors of the IT industry or professional services like architecture and law require liability insurance as a condition of practice. This requirement is in place to protect both the professionals and their clients from the financial fallout of any errors, negligence, or accidents.

Also read The Complete Guide to Hiring JavaScript Developers in India - Wisemonk.

What are the Cost Factors for Liability Insurance?

In today's litigious business environment, remote workers providing professional services are vulnerable to costly lawsuits from dissatisfied clients. A single E&O claim, even if unwarranted, can financially devastate an independent professional. For remote workers facing an errors and omissions lawsuit, errors and omissions(E&O) insurance typically covers:

- Attorney fees and legal defense costs

- Court costs and other legal expenses

- Settlements and judgments

- Disciplinary proceedings from professional boards

- Lost wages for time spent defending the claim

Without E&O coverage, remote service providers would have to pay these substantial costs out-of-pocket, putting their business and personal assets at risk.

Understanding the cost factors for liability insurance can help you make informed decisions that protect your business without breaking the bank. The cost of liability insurance can vary significantly depending on several factors. Here’s an overview of the key cost factors, typical cost estimates for different professions, and tips for managing your insurance expenses.

- Profession Type:

Professions with higher perceived risks, such as construction contractors or medical consultants, typically face higher premiums than lower-risk professions like freelance writers or graphic designers.

- Business Size:

The size of your business, in terms of both revenue and the number of employees, can also impact your insurance costs. Larger businesses require higher coverage limits, leading to increased premiums.

- Location:

Your geographical location can influence insurance costs as well. Areas with higher litigation rates or stricter regulatory requirements may see higher premiums. For example, a contractor in a metropolitan area might pay more than one in a rural location due to the increased likelihood of claims.

- Risk Level:

The specific risks associated with your business, such as the potential for client lawsuits, property damage, or professional errors, play a crucial role in determining your premiums.

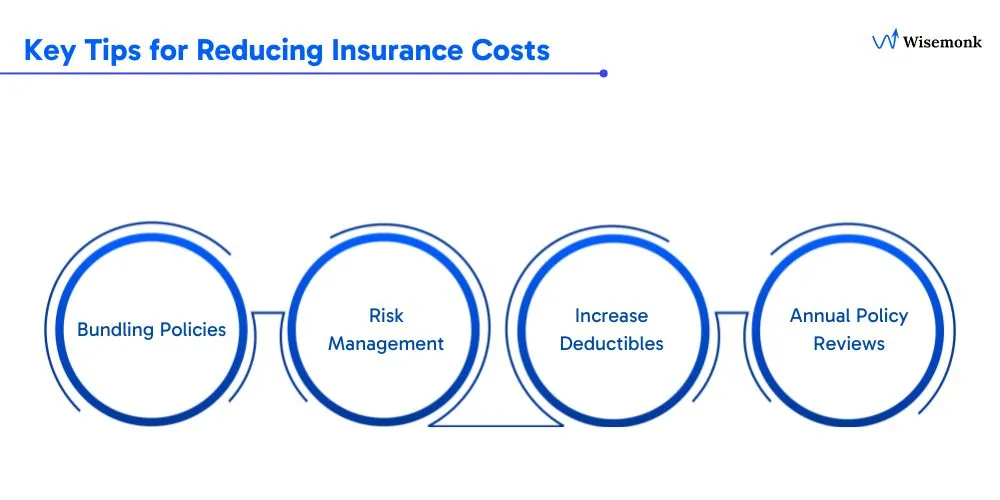

Key Tips for Reducing Insurance Costs

Bundling Policies:

Many insurance providers offer discounts if you bundle multiple types of coverage, such as general liability, professional liability, and property insurance, into a single package. This approach simplifies policy management and also leads to significant cost savings.

Risk Management:

Implementing strong risk management strategies can help lower your premiums. This includes maintaining safe work practices and using contracts that clearly outline the scope of work and client responsibilities. Also, keep detailed records of all transactions and communications.

Increase Deductibles:

Choosing a higher deductible can reduce your premium costs. However, ensure that the deductible is an amount you can comfortably afford in the event of a claim.

Annual Policy Reviews:

Regularly reviewing your insurance policy can help identify areas where you might be over-insured or opportunities to adjust coverage based on changes in your business. Adjusting your coverage to better match your current risk level can reduce unnecessary expenses.

By understanding these cost factors and employing strategies to manage and reduce them, you can secure the liability insurance coverage you need at a price that fits your budget.

How to Obtain Independent Contractor Liability Insurance?

A systematic approach can ensure that you’re adequately protected while also getting the best value for your money. Here’s a step-by-step guide on how to obtain independent contractor liability insurance.

The first step in obtaining liability insurance is to assess the specific risks associated with your profession.

- Identify Potential Liabilities: Consider the nature of your work and the common risks you might encounter. This includes understanding potential client claims, property damage, bodily injury risks, or professional errors.

- Evaluate Your Business Needs: Determine the type and amount of coverage needed based on the risks identified. For example, a general liability policy might be sufficient for some contractors, while others might need additional coverage.

- Consult with a Professional: If you’re unsure about the coverage you need, consulting with an insurance agent can provide valuable insights. They can help you tailor a policy that addresses your specific risks and business needs.

Once you’ve determined your coverage needs, the next step is to compare different insurance providers to find the best rates and coverage options.

- Research and Gather Quotes: Start by gathering quotes from multiple insurance providers. Look for companies that specialize in liability insurance for independent contractors.

- Compare Coverage Options: Don’t just focus on the cost of the premiums. Compare the coverage options offered by each provider, including the types of claims covered, coverage limits, and any additional benefits.

- Check Customer Reviews and Ratings: Look for reviews and ratings from other contractors to gauge the reliability and customer service of the insurance providers. This can give you an idea of how the company handles claims and supports its policyholders.

After selecting a provider, it’s essential to thoroughly understand the terms of the policy you’re purchasing.

- Review Policy Terms: Carefully read through the policy terms and conditions. Ensure you understand what is covered and, equally important, what is excluded.

- Know Your Coverage Limits: Coverage limits refer to the maximum amount your insurance will pay out in the event of a claim. Make sure the limits are sufficient to cover potential liabilities.

- Consider Deductibles: A deductible is the amount you’ll need to pay out of pocket before your insurance kicks in. Policies with higher deductibles have lower premiums, but it’s important to choose a deductible you can afford to pay if needed.

- Understand Renewal Terms: Some policies may have specific renewal terms or conditions. Make sure you’re aware of these to avoid lapses in coverage.

Taking the time to identify your risks, compare providers, and fully understand your policy will help you make an informed decision and secure the best possible coverage.

Benefits of Contractor Liability Insurance

Independent contractors juggle multiple responsibilities, from managing client relationships to delivering quality work on time. Amid these demands, it's easy to overlook the importance of liability insurance. However, the benefits of having this protection go beyond just mitigating risks—they also enhance your professional standing and can lead to significant cost savings. Let’s explore some key benefits of independent contractor liability insurance:

Financial Protection

One of the most significant benefits of liability insurance is the financial protection it offers against lawsuits and claims. As an independent contractor, you are personally responsible for any legal claims made against your business. Without insurance, the costs of legal defense, settlements, or damages can be overwhelming, potentially jeopardizing your financial stability. It allows you to focus on your work without the fear of financial ruin.

Professionalism and Credibility

Having liability insurance can enhance your professionalism and credibility in the eyes of potential clients. It signals that you are serious about your business and are prepared to take responsibility for your work. Many clients, especially larger companies, prefer to work with contractors who have liability insurance because it provides them with an additional layer of protection. This can give you a competitive edge when bidding for contracts or negotiating deals.

Cost Savings

Many insurance providers offer the option to bundle different types of insurance policies, such as general liability and professional liability, into one comprehensive package. Bundling can lead to significant cost savings compared to purchasing individual policies separately. This makes managing your insurance simpler and also ensures you are comprehensively covered across multiple areas of risk.

Focus on Core Work

Knowing that you are protected against potential risks and liabilities allows you to focus more on your core work and less on potential what-ifs. This peace of mind is invaluable. It frees up mental and emotional energy that you can redirect towards improving your services and achieving your professional goals.

Protection of Personal Assets

For independent contractors, the line between personal and business finances can often blur. Without liability insurance, your assets—such as your home, savings, or investments—could be at risk if a legal claim is made against your business. Liability insurance acts as a buffer, protecting your assets from being used to satisfy business-related liabilities.

Looking for top-notch professionals to elevate your business? Discover the exceptional talent India has to offer! Connect with talented independent contractors who can bring your projects to life with innovation and expertise.

Explore Now to find the perfect match for your business needs and unlock unparalleled success.

Conclusion

Currently, standalone professional liability insurance has a very low penetration in India compared to developed markets. Lack of awareness among professionals is a key challenge.

Insurers and brokers need to educate remote workers and freelancers about professional liability risks and the importance of proper coverage. Offering affordable premiums and convenient digital distribution can also improve adoption.

As remote work continues to grow in India, having professional liability coverage will become a key consideration for independent workers to safeguard their interests. It not only provides financial protection but also enhances credibility and trust with clients.

In conclusion, professional liability insurance is an essential risk management tool for remote workers and contractors. As India's gig economy expands, this segment presents a significant growth opportunity for liability insurers in the coming years.

If you haven’t already, now is the time to take the necessary steps to protect your business from unforeseen risks. Don’t wait until it’s too late—secure liability insurance that suits your specific needs and provides comprehensive protection. Your business deserves the best chance to thrive, free from the financial burdens of potential claims and lawsuits.

How can WiseMonk Help?

When it comes to finding the right liability insurance, WiseMonk is an invaluable resource for independent contractors. Here’s how we can help:

- Tailored Insurance Solutions: We offer insurance options specifically designed for independent contractors, ensuring you get coverage that matches your unique risks and needs.

- Competitive Rates: By comparing multiple insurance providers, WiseMonk helps you find the best rates and coverage options, so you don’t have to overspend to protect your business.

- Expert Guidance: With a deep understanding of the independent contractor landscape, we provide expert advice to help you make informed decisions about your insurance needs.

- Streamlined Process: Getting insured can be a hassle, but WiseMonk simplifies the process, making it easy to find and secure the right coverage quickly and efficiently.

Take the first step towards protecting your business today by exploring the insurance options available at WiseMonk. Your business is worth it!

Frequently asked questions

What does independent contractor liability insurance cover?

It typically covers legal fees, settlements, and damages if a client claims financial loss or injury due to your work. Coverage can include general liability, professional liability, and errors & omissions insurance depending on the profession.

Is liability insurance mandatory for independent contractors?

While not legally required in all industries, many clients demand proof of insurance before awarding contracts. It reduces financial risk and provides protection against lawsuits or accidental damages.

How much does independent contractor liability insurance cost annually?

Costs vary based on industry, coverage limits, and risk level, but most policies range between $500 and $2,500 per year. High-risk professions like construction may pay higher premiums than consulting or IT services.

Can independent contractors get liability insurance for short-term projects?

Yes, many insurers offer short-term or project-based liability coverage. These policies provide protection for the specific duration of a contract, often at a lower cost than annual plans.

Does liability insurance cover remote work?

Yes, as long as the policy includes coverage for work performed outside traditional office settings. Contractors should confirm with their insurer that remote services are included in their policy.

What professions benefit most from liability insurance?

Professions like IT consulting, marketing, healthcare, design, and construction often require liability coverage due to the higher risk of client claims. Any role involving advisory services or physical work benefits from protection.

How do I choose the right contractor liability insurance policy?

Compare policies based on coverage limits, exclusions, premium costs, and insurer reputation. Working with a broker or specialized provider ensures tailored coverage for your specific profession and risk profile.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20in%20India.webp)

.webp)

.webp)

%20(3).webp)

.webp)

.webp)

.webp)

.webp)

.webp)